- 877-241-5144

- M-F: 8am to 8pm

ACE + PDR Freddie Mac Eligible Loans

Home » Services » Residential Appraisals » ACE + PDR Freddie Mac Eligible Loans

Fast Turn Times With ACE + PDR Freddie Mac Eligible Loans

When lenders need a faster alternative to a traditional appraisal, ACE + PDR may provide the solution. For certain Freddie Mac eligible loans, this process allows transactions to move forward without ordering a full appraisal report. Instead, lenders rely on verified property data and Freddie Mac’s automated evaluation system.

At AmeriMac, we coordinate the entire process nationwide. From ordering property data collection to helping ensure eligibility standards are met, our team supports lenders every step of the way. Our team in New Albany, OH, delivers consistent turn times and dependable service.

What Is ACE + PDR?

ACE + PDR is an alternative to a traditional appraisal for certain Freddie Mac loans. When a loan qualifies, lenders can proceed without a full appraisal report.

Instead of relying on a licensed appraiser’s written value opinion, the process uses verified property data and Freddie Mac’s automated system to determine eligibility. The goal is to reduce delays while maintaining underwriting standards.

What You Need To Know

An ACE + PDR can be ordered through AmeriMac nationwide

Freddie Mac reviews available property data and overall loan risk to determine whether the loan qualifies. When eligibility standards are met, the system may allow the transaction to move forward without a traditional appraisal.

If required, a Property Data Report includes verified information about the home. This supports the automated review process and helps eliminate the need for a full appraisal report.

How ACE + PDR Works

Freddie Mac evaluates the property and loan details through its automated system. If the loan meets the required guidelines, a traditional appraisal may not be needed.

When a Property Data Report is required, a trained data collector gathers information such as:

- Interior and exterior photos

- Square footage measurements

- Room counts

- Floor plan layout

- Property condition details

This verified information allows the loan to proceed without requiring a full appraisal report.

Unlike a hybrid appraisal, ACE + PDR does not require an appraiser to produce a signed property valuation report when eligibility is confirmed.

The AmeriMac Commitment

- Qualified property data collectors trained on Freddie Mac’s PDR standards.

- Flat nationwide fee of $225

- Typical turn time of 2-3 business days*

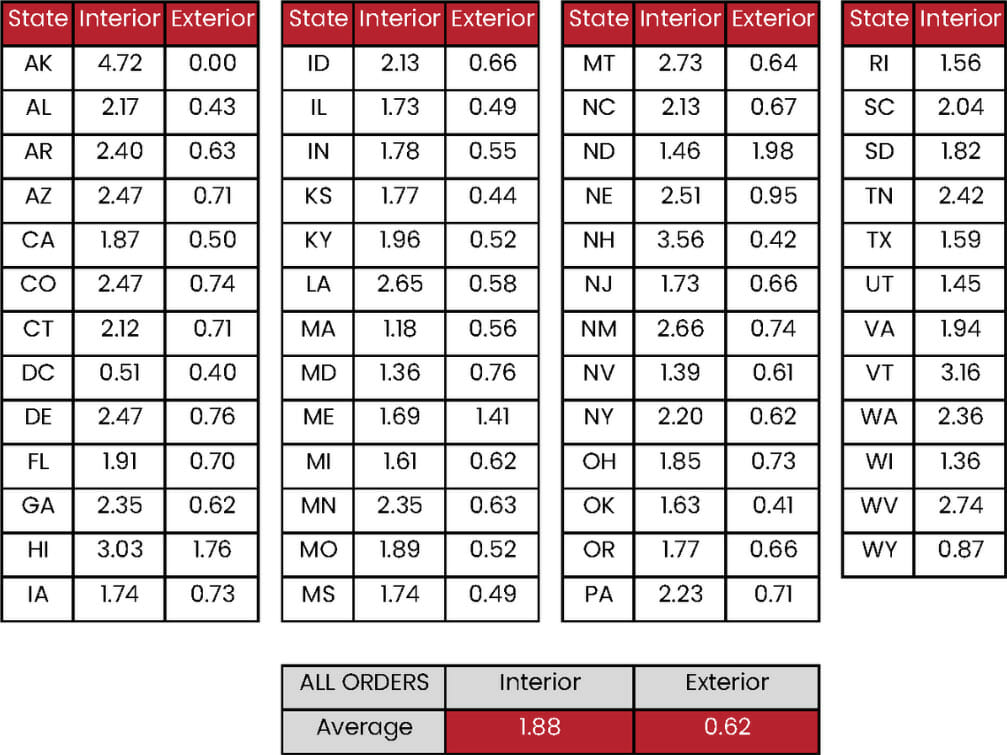

Example Turn Times

The following averages reflect recent interior and exterior collection timeframes by state.

Because this process operates in place of a traditional appraisal, lenders often experience shorter turnaround times and fewer scheduling delays.

How ACE + PDR Differs From a Traditional Appraisal

A traditional appraisal requires a licensed appraiser to inspect the property and prepare a signed report that includes comparable sales and a value conclusion.

ACE + PDR works differently. Instead of producing a full appraisal report, the process relies on verified property data and Freddie Mac’s automated evaluation system to determine eligibility.

This also differs from a hybrid appraisal, which still requires an appraiser to review data and issue a report. ACE + PDR removes that step when the loan qualifies.

Eligible Loans and Transaction Types

Freddie Mac eligible loans that may qualify include:

- Eligible purchase transactions

- Rate-and-term refinances

- Limited cash-out refinance loans

Eligibility depends on the property, transaction type, and overall loan profile. Not all properties qualify, so lenders should confirm eligibility before proceeding.

The Role of Property Data Collectors

Property data collectors play an important role in the PDR process at Freddie Mac. These professionals gather accurate property information but do not provide an opinion of value. Their work supports the automated collateral evaluation. The information they collect supports Freddie Mac’s automated review process. This ensures consistency across transactions. Unlike appraisers in traditional or hybrid appraisals, property data collectors focus solely on factual data collection.

Benefits of ACE for Lenders

There are several benefits of ACE within the mortgage industry.

Faster Turn Times

Without a traditional appraisal report, lenders avoid scheduling delays, revision cycles, and appraisal review bottlenecks. This can accelerate underwriting timelines and improve borrower experience.

Cost Predictability

A flat, standardized fee provides consistency across markets. Lenders gain clearer margin control compared to variable traditional appraisal pricing.

Reduced Administrative Burden

Because no full appraisal report is generated, lenders eliminate appraisal review management and collateral condition adjustments tied to value disputes. This simplifies internal processing and quality control workflows.

Risk-Based Automation

Freddie Mac’s ACE evaluates overall underwriting risk using established valuation models and historical data. This supports consistent decision-making across loan files.

Integrated Workflow With Loan Product Advisor

ACE eligibility is delivered directly through the Loan Product Advisor and confirmed via the LPA feedback certificate. This creates a streamlined valuation process that aligns with existing underwriting systems.

How AmeriMac Helps Lenders

AmeriMac supports lenders by:

- Monitoring LPA feedback certificate results

- Coordinating property data collection nationwide

- Ensuring compliance with Freddie Mac’s property eligibility requirements

- Managing communication with property data collectors

- Delivering consistent collateral data

Recent Updates and Compliance Considerations

Freddie Mac periodically updates its guidelines and eligibility standards. These updates may affect appraisal waiver availability and property requirements. Lenders should review official Freddie Mac resources for the most current guidance. We remain aligned with evolving standards to help ensure smooth implementation.

Frequently Asked Questions

Freddie Mac may offer an ACE appraisal waiver when the Loan Product Advisor determines the loan meets specific risk and collateral criteria. Eligibility depends on additional property information, transaction type, and overall underwriting profile. The LPA feedback certificate will confirm whether ACE is available.

Loans may be ineligible due to property condition concerns, incomplete data, higher risk classifications, or certain transaction characteristics. Unique or complex properties may also fall outside eligibility standards. Lenders should review the current Freddie Mac property eligibility requirements before proceeding.

Not always. In some cases, ACE may be issued without requiring a PDR. However, if the Loan Product Advisor generates a PDR offer, verified property data collection must be completed before the loan can proceed without a traditional appraisal.

Eligibility varies based on Freddie Mac guidelines and the specific loan profile. Some investment properties may qualify if they meet collateral and risk standards. Lenders should confirm eligibility through the Loan Product Advisor.

Partner With AmeriMac for ACE + PDR Support

ACE + PDR represents continued modernization within the mortgage industry. By combining automated collateral evaluation with structured property data collection, lenders gain an efficient alternative to traditional appraisal workflows.

At AmeriMac, we coordinate the full process from data collectors to compliance alignment. Our goal is to help lenders confidently execute Freddie Mac eligible loans with reliable turn times and consistent service.

Contact AmeriMac today to learn how we can support your collateral workflow.

10 Reasons to Choose AmeriMac

Our Appraisal Ordering Process

Our Commitment to Compliance

Read Our 5-Star Reviews

Connect with AmeriMac Appraisal Management Today

The fully staffed customer service department at Amerimac Appraisal Management is available Monday through Friday, 8 a.m. EST to 8 p.m. EST.

SIGNUP FOR OUR MONTHLY NEWSLETTER:

© Amerimac 2026. Privacy Policy. Website by WMx Digital.